How Payment Processing Works: Learn the 3 P's of payment processing.

Players.

There are three main players when it comes to processing credit and debit card payments, whether online, via phone sales, or even in person. On one end is you, the business owner or merchant. On the other end is your customer. And in between is a lot of technology that connects the two of you.

1. You, the merchant.

In order to accept credit and debit card payments from online customers, you’ll need to partner with some key players. As a business owner, it’s likely you’ll need a merchant bank (sometimes called an acquirer) that accepts payments on your behalf and deposits them into a merchant account they provide.

In order to accept credit and debit card payments from online customers, you’ll need to partner with some key players. As a business owner, it’s likely you’ll need a merchant bank (sometimes called an acquirer) that accepts payments on your behalf and deposits them into a merchant account they provide.

2. Your customer.

Similarly, in order for your customer to pay for your goods and services, she needs a credit or debit card. The bank that approves her for the card (and lends her the cash to pay you) is called the issuing bank.

Similarly, in order for your customer to pay for your goods and services, she needs a credit or debit card. The bank that approves her for the card (and lends her the cash to pay you) is called the issuing bank.

3. The technology.

In the middle are two technologies that enable you and your customer to transact. The first is the payment gateway, software that links your site’s shopping cart to the processing network. The second is the payment processor (or merchant service), which does all the heavy lifting: moving the transaction through the processing network, sending you a billing statement, working with your bank, etc. Often, your merchant bank is also your payment processor, which helps simplify things.

In the middle are two technologies that enable you and your customer to transact. The first is the payment gateway, software that links your site’s shopping cart to the processing network. The second is the payment processor (or merchant service), which does all the heavy lifting: moving the transaction through the processing network, sending you a billing statement, working with your bank, etc. Often, your merchant bank is also your payment processor, which helps simplify things.

Online payments.

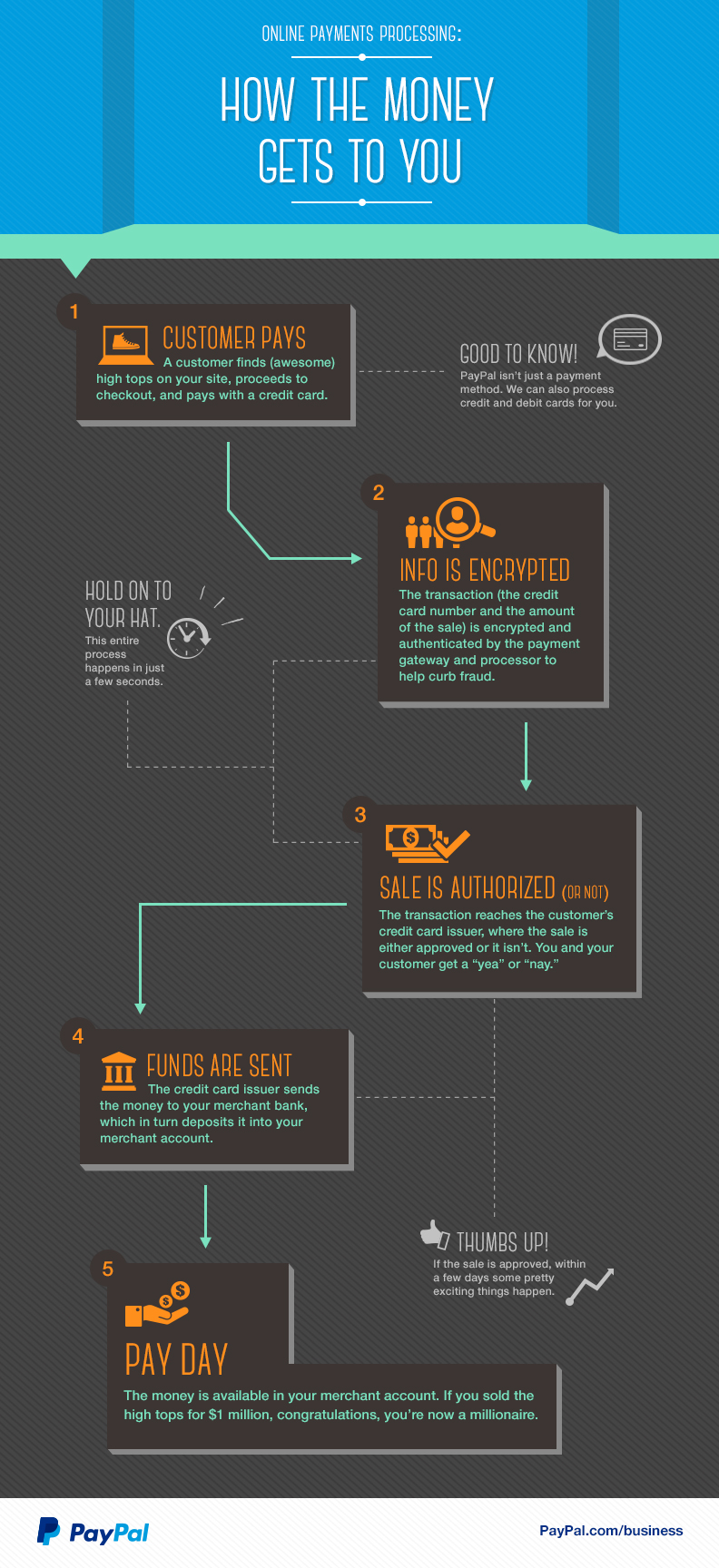

As a business owner, it’s helpful to understand exactly how money moves from your customer to your business. There are two stages to payment processing: the authorization (approving the sale) and the settlement (getting the money in your account).

The authorization process goes roughly like this:

1. Your customer buys an item on your site with a credit or debit card.

2. That information goes through the payment gateway, which encrypts the data to keep it private, and sends it to the payment processor.

3. The payment processor sends a request to the customer’s issuing bank to check to see that they have enough credit to pay for your stuff.

4. The issuer responds with a yes (an approval) or a no (a denial).

5. The payment processor sends the answer back to you that the sale was approved and also tells your merchant bank to credit your account.

All of the above takes place within one to two seconds.

The second piece of the process (where you get paid!) is the settlement:

1. The card issuer sends the funds to your merchant bank, which deposits the money into your account.

2. The funds are available.

The settlement process can take a few days. Sometimes, your bank lets you access your money before it’s even sent to them. They also might keep a portion in your account that you can’t touch, just in case the customer returns things later (called a reserve in payments speak).

Pricing.

We’ve learned about how payments come in, but what about the other side of the coin? What will it cost? As you might’ve guessed, everyone who touches the transaction wants to get paid, including the issuing bank, the credit card association (Visa, MasterCard, etc.), the merchant bank, and the payment processor.

At its most basic, every time you process a sales transaction, you pay four fees:

- A percent of the transaction amount: The issuer gets paid by taking a percentage of each sale, called the interchange. This fee varies depending on a bunch of things, such as industry, sale amount, and type of card used.

- Another percent of the transaction amount: The credit card association (Visa, MasterCard, etc.) also charges a fee, called an assessment.

- Yet another percent of the transaction amount: Your merchant bank takes a cut by charging you a percentage fee. The amount here also varies by industry, amount of sale, monthly processing volume, etc.

- A dollar amount for every transaction processed: The payment processor (who might also be your merchant bank) makes money by charging a fee, called an authorization fee, every time you process a transaction (whether it’s a sale, a decline, or a return – no matter). Plus, it can charge fees for setup, monthly usage, and even account cancellation.

Usually, the first three fees (the percentages) are all added together and quoted as a single rate, while the transaction fee is quoted separately (e.g., 2.9% + $0.30).

Complicating the picture, most pricing structures generally fall into one of three categories:

- With flat-rate pricing, you pay a fixed percent for all transaction volume, no matter what the actual costs are. All of the above fees are baked into this single rate. For example, you are charged a bundled rate of 2.9% of the transaction amount + $0.30 per transaction. On a $100 sale, the fee you pay works out to be $3.20.

- With interchange plus pricing, your merchant service charges you a fixed fee on top of the interchange. For example, 2.0% + $0.10 on top of a 1.8% interchange fee. On a $100 sale, that works out to be a $3.90 fee. Of course, remember that there are 300 or so different interchange fees, so the 1.8% can vary wildly!

- In tiered pricing, the processor takes the 300 or so different interchange rates and lumps them into three buckets (or pricing tiers): qualified, mid-qualified, and nonqualified. This makes it simpler for you (and them) to understand. However, because the processor defines the buckets any way it wants, it can be expensive. As an example, the fees you pay on a $100 sale could range from $2.50 to $3.50, depending how it has been classified.

Whether you’re expanding a brick-and-mortar business to accept payments online or starting a new venture from the ground up, it’s important to know how online payments, players, and pricing work before the first customer hits "check out." That way, you’ll be prepared with a plan that works best for you and your business.